Arm vs. Qualcomm: Consistent Growth vs. Revenue Volatility

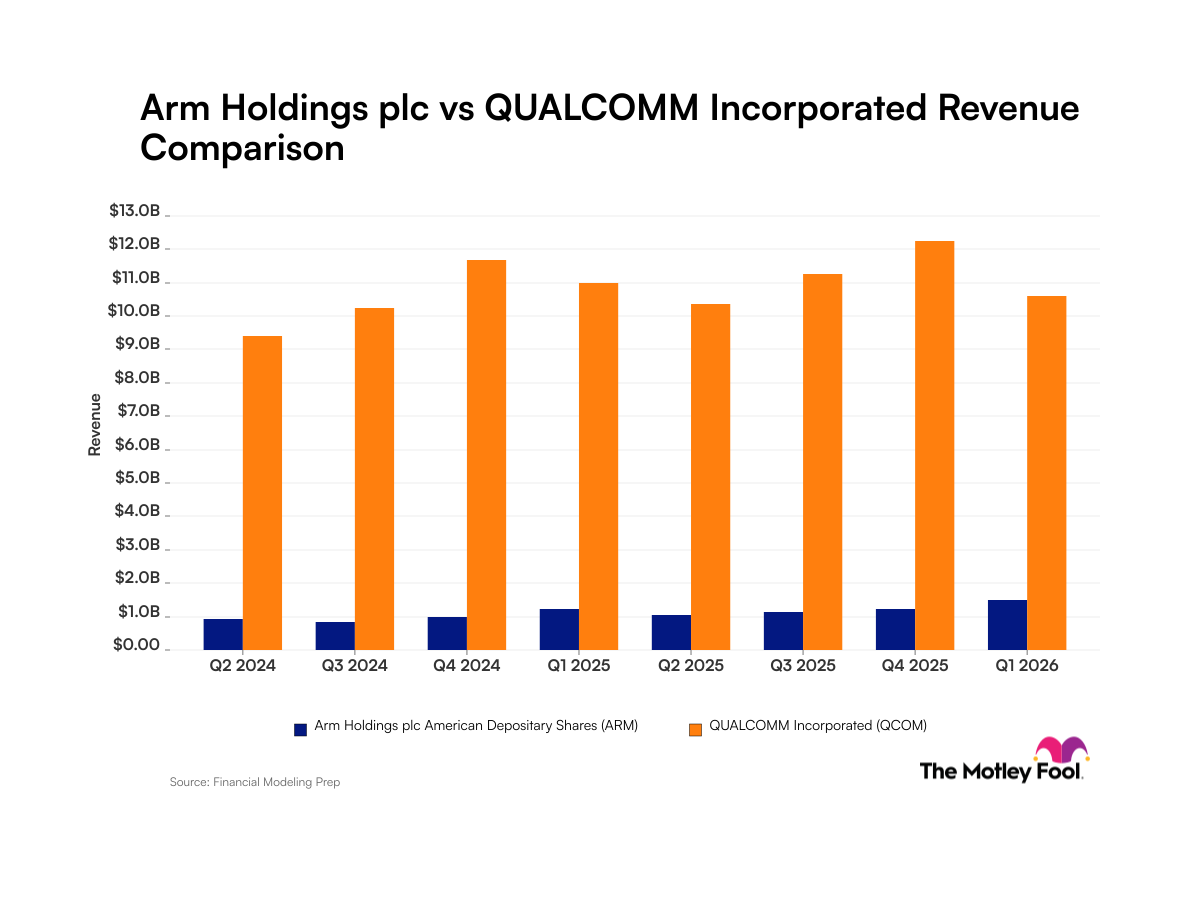

Arm vs. Qualcomm spotlights two semiconductor peers with expanding AI opportunities and contrasting growth trajectories. Arm Holdings shows steady momentum, with revenue up 20% year over year in Q1 2026 and a 21% net income margin, driven by licensing and royalties on CPU designs. Qualcomm, shifting away from handsets toward automotive, IoT, and data centers, posted revenue a eventful -3.5% year over year in Q1 2026 but delivered a net margin near 70%. Over the past three years, Arm has surged roughly 600% in stock value versus about 123% for Qualcomm, reflecting different investor perceptions of scalable AI opportunities. Arm relies on licensing and royalties for chip designs, positioning it to benefit as AI agents increase CPU demand in automotive and consumer devices. Qualcomm is pivoting to data centers and AI-powered devices, including smart glasses, while maintaining profitability around the 70% net margin. Analysts will watch whether Qualcomm accelerates revenue growth as its strategic shift unfolds, or if Arm continues to grow faster and narrows the gap.